Car purchase for Ego or income: Vietnamese lack the financial literacy to make an informed decision, leading to bitter regrets

For most Vietnamese families, buying a car is the ultimate symbol of success, freedom, and providing for the family. However, a sparkling showroom moment can quickly give way to intense financial regret.

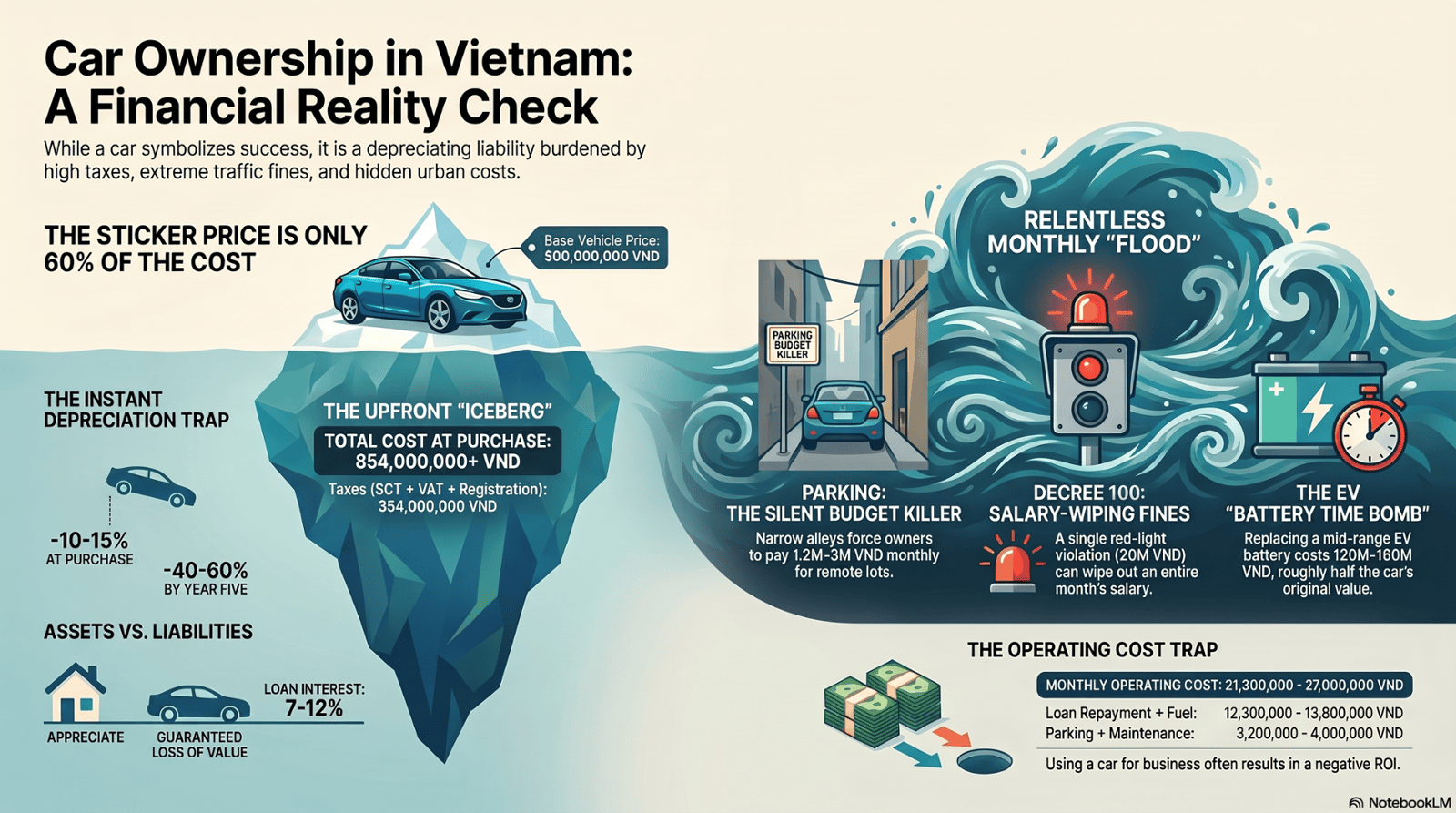

As detailed in Risk Finance car owner in VN.pdf, a critical lack of education regarding vehicle depreciation, hidden registration taxes, and high-interest commercial bank loans (ranging from 7% to 12%) is trapping buyers in a relentless monthly cash drain. Instead of the car working for the family, unprepared owners end up working just to serve the car.

You bought a car in Vietnam.

Now protect it — wisely.

Before the first traffic fine lands, before the monsoon season arrives, before the next congested roundabout — here is everything you need to know about car insurance in Vietnam and how to get the best deal from the market's leading insurers.

In our previous piece, we showed that owning a car in Vietnam costs far more than the sticker price. But there is one category of cost where spending too little can be catastrophic: insurance. Getting it wrong — or skipping it — can turn a minor fender-bender into a financial crisis.

The two types of car insurance you need to understand

Vietnamese law draws a very clear line between two categories of car insurance, and understanding that line will determine whether you are legally compliant and financially protected.

1. Compulsory civil liability insurance (bảo hiểm TNDS bắt buộc)

This is the legal minimum. Every vehicle on Vietnamese roads must carry it. It covers damage you cause to third parties — other people's vehicles, property, and medical costs. The premiums are low, government-regulated, and non-negotiable. Driving without it is a fineable offence.

Coverage limits under the compulsory scheme: up to 150 million VND per person for bodily injury and 50 million VND for property damage per incident. In a serious accident in Ho Chi Minh City's congested traffic, those limits can be exhausted alarmingly quickly.

2. Voluntary comprehensive insurance (bảo hiểm vật chất xe)

This covers your own vehicle. It is optional — but, as we will explain, effectively essential for anyone with a car worth over 200 million VND or anyone using their car for commercial purposes. This is where the real financial protection lives, and where the choice between insurers matters enormously.

The compulsory minimum protects others, not you. If your car is totalled, stolen, or damaged in a flood — none of that is covered by the legal minimum. Without a voluntary policy, you bear 100% of repair or replacement costs personally.

Why Vietnam's roads make comprehensive cover non-negotiable

Vietnam's traffic environment creates a distinctive risk profile that makes thorough insurance coverage especially important. These are the specific risks your policy must address:

The real cost of a comprehensive policy in Vietnam

Comprehensive (vật chất) premiums in Vietnam are typically calculated as 1% to 1.6% of the vehicle's insured value per year, with variations based on vehicle age, usage type, driver profile, and insurer. Here is a realistic cost breakdown for three common vehicle categories:

| Vehicle type | Insured value | Est. annual premium |

|---|---|---|

| City car (VinFast VF 3, Toyota Vios) | 320–500 million VND | 3.2–8 million VND |

| Mid-size SUV (Hyundai Tucson, Ford Territory) | 700 million – 1.1 billion VND | 7–17.6 million VND |

| Premium EV (VinFast VF 8, VF 9) | 1.2–1.7 billion VND | 12–27.2 million VND |

| Commercial / ride-hailing use (+30–50% loading) | Any | +30% to +50% on above |

| Compulsory TNDS (all vehicles) | Regulated | ~600,000 VND fixed |

Most Vietnamese insurers offer deductible options from 0 to 3 million VND per claim. A higher deductible lowers your annual premium by 15–30% — but requires you to absorb the first portion of any repair. For low-mileage leisure drivers, a 2–3 million VND deductible can meaningfully reduce annual costs. For daily commuters or ride-hailing drivers who file more frequent small claims, a zero-deductible policy may cost less over time. This is exactly the type of calculation where professional advice pays for itself.

Three leading Vietnam insurers compared

The Vietnamese insurance market for motor vehicles is dominated by domestic players licensed by the Ministry of Finance. Here is a comparative snapshot of three strong options — and why the differences between them matter more than most buyers realize.

Premium rates alone do not tell the full story. What matters just as much — especially when you actually need to make a claim — are the details buried in the policy terms:

- Flood and water damage coverage: Critical in Vietnam's monsoon climate. Check whether the policy covers engine damage from driving through floodwater — some policies exclude this as "driver negligence."

- Total loss valuation method: Is your car insured at agreed value or market value? After depreciation, market value payouts can fall far short of what you need to replace the vehicle.

- Garage network and cashless repair: Some policies require you to pay the repair shop and claim reimbursement. Others offer direct billing to authorized garages — far more convenient after an accident.

- EV battery coverage: Not all policies cover EV battery replacement at full value after a collision. With replacement costs of 68–200 million VND, this exclusion is financially catastrophic for EV owners.

- Commercial use exclusion: Most standard policies void coverage if the vehicle is used for Grab, Be, or Xanh SM without a specific commercial rider. Ride-hailing drivers must declare their usage — and pay the loading accordingly.

- Driver restriction clauses: Policies that cover only the named driver create problems if family members or employees also use the vehicle regularly. Named-driver versus any-qualified-driver policies differ in premium and flexibility.

An independent insurance broker can access policy terms across all three (and more) Vietnamese insurers simultaneously — and negotiate on your behalf. They are paid by the insurer, not you, so the advice costs nothing. What you gain is a side-by-side comparison of the clauses that matter: deductibles, flood exclusions, EV battery coverage, and commercial use riders. A small policy difference in these clauses can mean tens of millions of dong in a real claim.

Get quotes from 3 Vietnamese insurers — side by side

Tell us your vehicle, usage type, and coverage needs. We run your profile against PVI, BIC, and PTI (plus other licensed Vietnamese insurers) and deliver a clear comparison of premiums, deductibles, and the clauses that matter — in under 24 hours.

The hidden cost that insurers don't advertise: the claims process

A policy's true value reveals itself only when you actually file a claim. Vietnam's major insurers have improved their claims handling significantly, but there are still wide variations in:

Claim settlement speed. Industry average for straightforward motor claims in Vietnam is 7–21 working days. Some insurers settle within 5 days for smaller claims with their own network garages; others take up to 30 days for total loss assessments. If your car is your income vehicle, every day off the road costs money.

Documentation requirements. Vietnamese insurers typically require: a police report (biên bản công an) for any incident involving third parties, original repair invoices, photographic evidence filed within 24–48 hours of the incident, and the vehicle registration certificate. Missing any of these can delay or void a claim.

Depreciation deductions. On older vehicles (over 3 years), some policies apply an annual depreciation rate of 10–15% to parts and labor costs. On a car worth 500 million dong in year five, a total loss payout could be calculated at 60–70% of replacement cost — not 100%.

Under Decree 168/2024 (effective January 2025), traffic fines for car drivers have increased dramatically. Running a red light: up to 20 million VND — and insurance does not cover traffic fines. However, if a fine-related accident causes third-party damage, your civil liability policy may still respond for the damage component. Understanding this boundary is essential: your insurer covers damage, not penalties.

Optimizing your policy: what a consultant actually does for you

Most car owners in Vietnam buy insurance the way they buy phone credit — quickly, cheaply, and without reading the details. A professional insurance consultant does something different. They match your specific risk profile to the policy structure that delivers the most efficient coverage for your situation.

Here is what that analysis looks like in practice:

For a leisure driver living in an apartment with secure parking, driving under 1,500 km/month, no commercial use: the priority is flood coverage, a competitive deductible of 1–2 million VND, and a fast cashless garage network. A consultant can identify which insurer offers the best combination of these factors for your specific vehicle model.

For a ride-hailing or taxi driver using the car 10+ hours per day: the compulsory policy must be supplemented by a commercial use rider (which most standard policies exclude). Premium loading of 30–50% applies, but the alternative — driving uninsured for commercial purposes — voids all coverage and creates unlimited personal liability. A consultant ensures the policy is properly structured to respond when a claim actually occurs.

For an EV owner (VinFast VF series, BYD, or other): the battery coverage clause is the most important single factor in the policy. A consultant will negotiate an explicit endorsement confirming that the battery is covered at replacement cost, not book value, including in flood damage scenarios. Without this, an EV owner with a flooded battery could receive a settlement that covers only a fraction of a 120–200 million VND replacement.

Speak to a Vietnam insurance consultant — at no cost to you

Our licensed advisors in Ho Chi Minh City and Hanoi specialize in motor insurance for Vietnamese market conditions. The consultation is free. The policies are competitively priced. The peace of mind is permanent.

The right policy costs less than

one uncovered repair.

Vietnam's roads are demanding. The right insurance structure turns an unpredictable risk into a managed, affordable cost. Let us match you with the best policy for your vehicle, your usage, and your budget — free of charge.